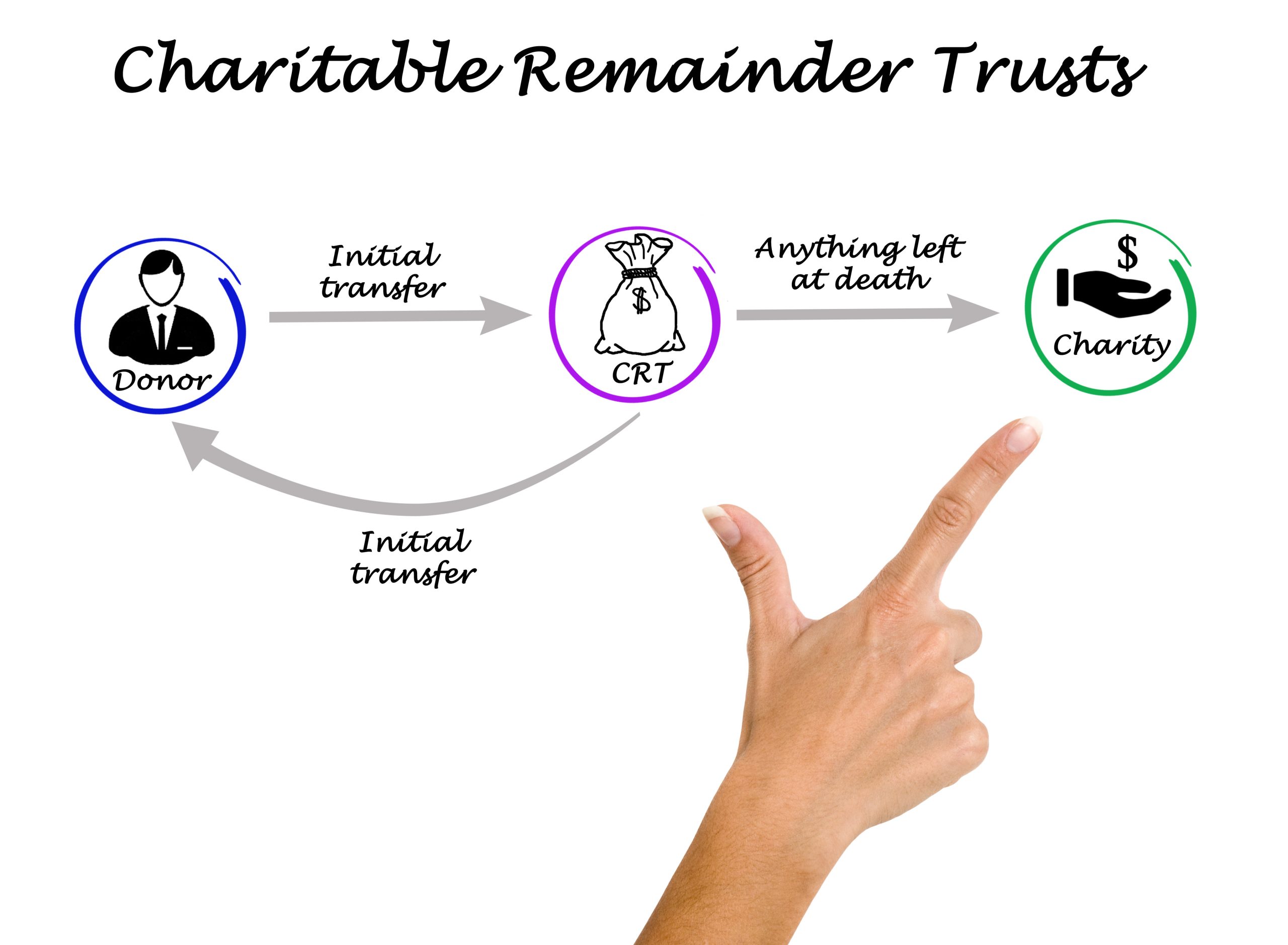

Generally speaking, almost any asset can be placed into a CRT, including real estate, stocks, bonds, mutual funds, and more. However, certain property types may not be eligible depending on their source or structure, so it’s important to consult with your advisor before transferring any asset into your trust.